Traditional 401(k) vs. Roth 401(k): Which Is Right for You?

If you’re a working professional saving for retirement, chances are most of your wealth is tied up in your 401(k). But one of the biggest questions we hear from clients is:

“Should I put money in a Traditional 401(k) or a Roth 401(k)?”

Both accounts are powerful tools — but the right choice depends on your income, tax situation, and future goals.

How They Work:

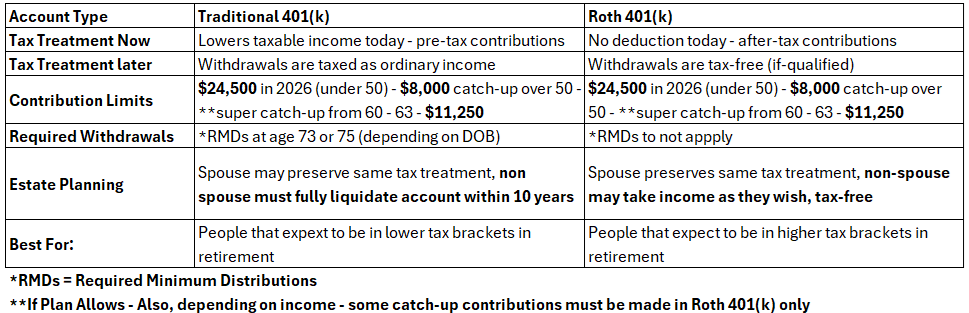

Traditional 401(k)

• Contributions: Made with pre-tax dollars

• Taxes: You get a tax deduction today, but every dollar you withdraw in retirement is taxed as ordinary income

• Best for: High earners who expect to be in a lower tax bracket when they retire

Roth 401(k)

• Contributions: Made with after-tax dollars

• Taxes: No tax deduction today, but withdrawals (including growth) are 100% tax-free in retirement

• Best for: Younger professionals or those who expect higher income/taxes in the future

The Key Differences

Conclusion: Should I Contribute to a Roth 401(k) or a Traditional 401(k)?

There’s no one-size-fits-all answer to the Roth vs. Traditional 401(k) debate. The best strategy depends on:

• Your current income and tax bracket

• Expected retirement lifestyle and expenses

• How much flexibility you want in the future

A thoughtful mix of both types of accounts often gives you the most control over your retirement tax picture.

If you’re unsure which option makes sense for your situation, consider working with a fee-only financial advisor who can run tax projections and create a personalized retirement strategy.